141:1 - The Math of Restraint

3 banks failed. VIX hit 30. The system stayed below critical escalation. The classification was right.

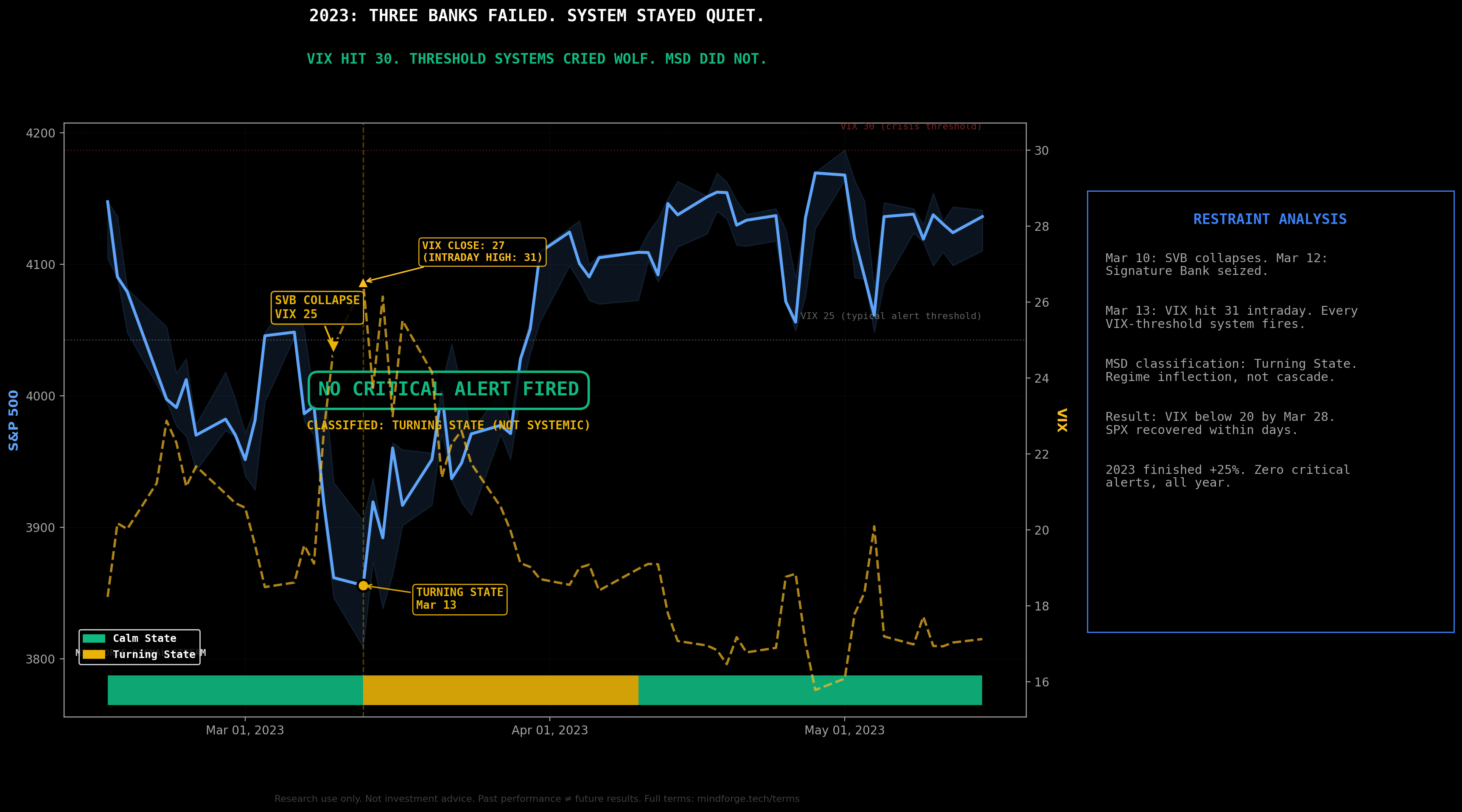

In March 2023, Silicon Valley Bank collapsed. Signature Bank followed. First Republic wobbled on the edge.

VIX hit 30. Headlines screamed banking crisis, contagion, systemic risk.

Our automated research system fired zero critical alerts.

Four months later, markets hit new highs. 2023 finished higher.

The system’s restraint matched the outcome.

The Math of Restraint

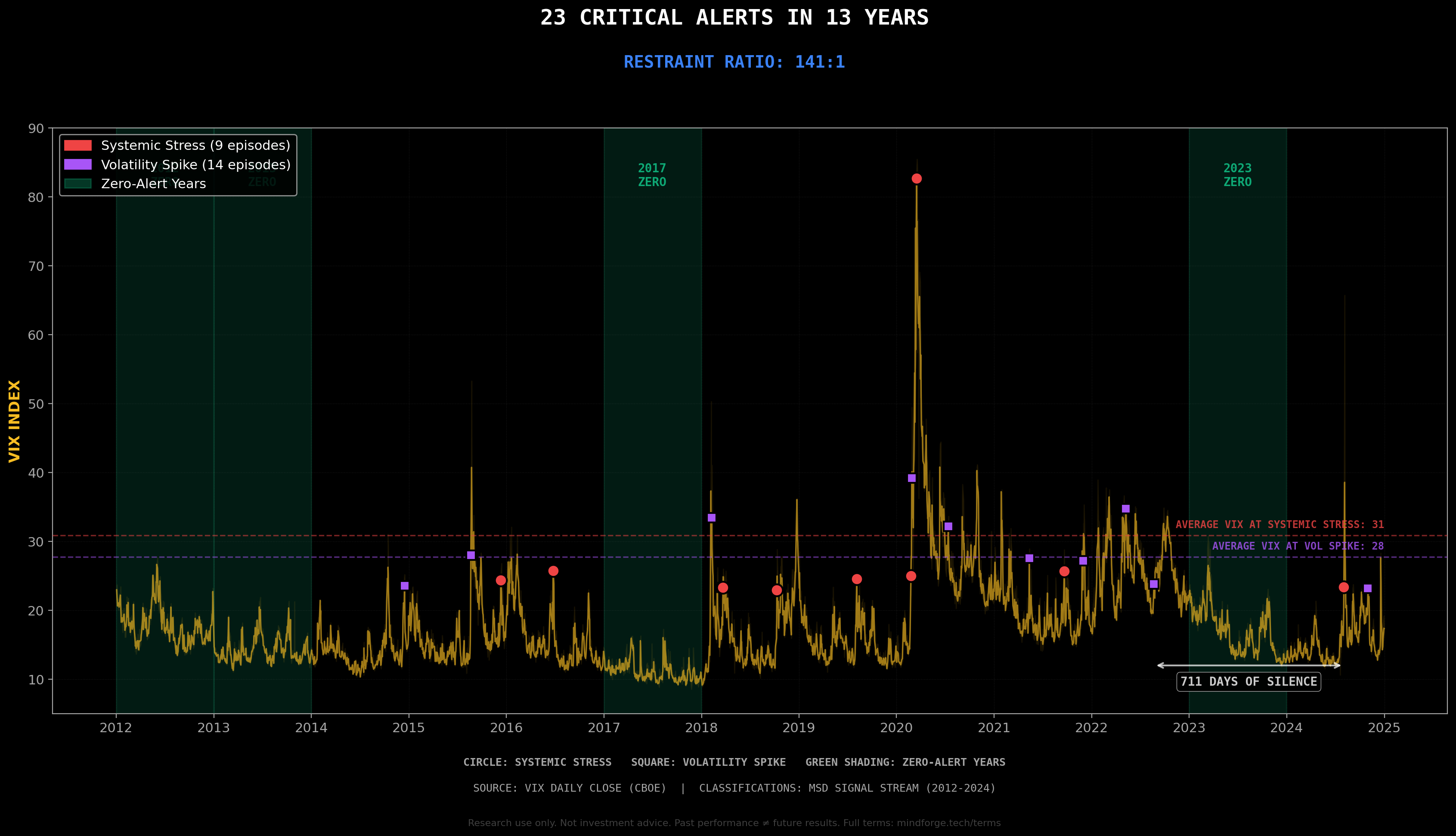

Over 13 years (2012–2024), our system analyzed approximately 3,276 trading days.

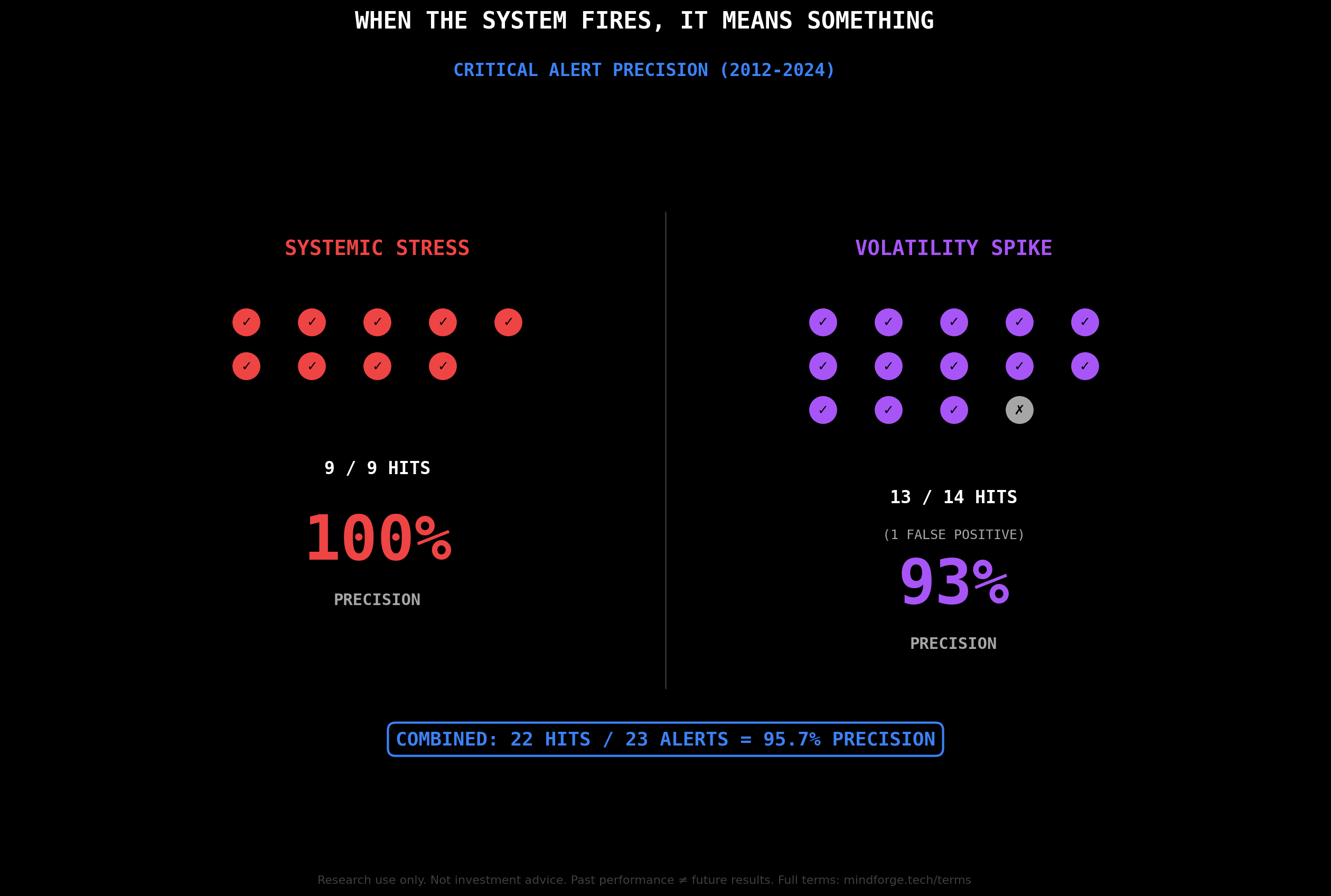

It fired 23 critical activations (Systemic Stress or Volatility Spike). Total.

That’s a 141:1 restraint ratio — roughly 141 trading days of restraint per critical activation.

In other words: for every day the system escalated to Critical, it correctly did not escalate on roughly 141 other trading days.

Note: Those 23 activations occurred across 19 unique trading days (some days triggered both critical states).

Getting “yes” right is table stakes. Any system can fire alerts.

Getting “no” right is harder. That’s where most systems fail.

The Years With Zero

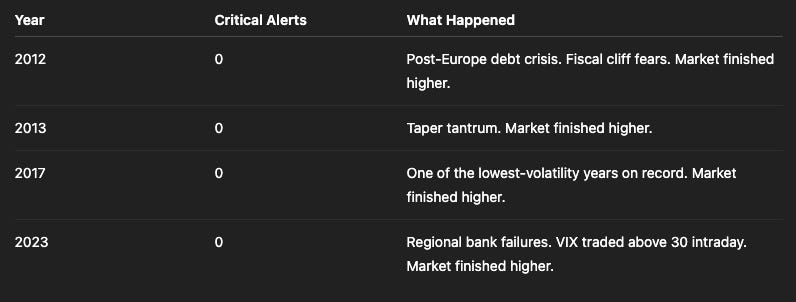

Four complete years with zero critical alerts.

2023 is the proof. Three major banks failed. VIX spiked. Every threshold-based system would have fired. Ours withheld the critical designation.

Why? Because elevated VIX isn’t the same as systemic crisis.

The broader environmental context didn’t match the cascade pattern.

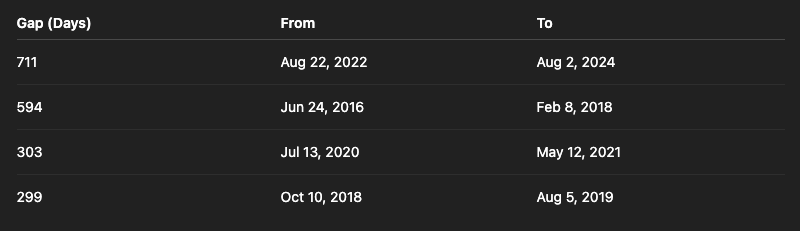

The Gaps Between Alerts

711 days. Nearly two years of silence on the critical channels (Aug 2022 → Aug 2024).

During that silence:

2023 bank crisis (VIX ~30)

Inflation fears

Fed hiking cycle

Multiple VIX spikes above 25

The system watched all of it. It measured the conditions, classified them as Turning or Stress (standard regime states), but never escalated to Critical.

Then on August 2, 2024, the yen carry trade unwound. The system classified Systemic Stress. The following trading session, VIX hit 65.

When a system stays quiet for 711 days and then fires, you pay attention.

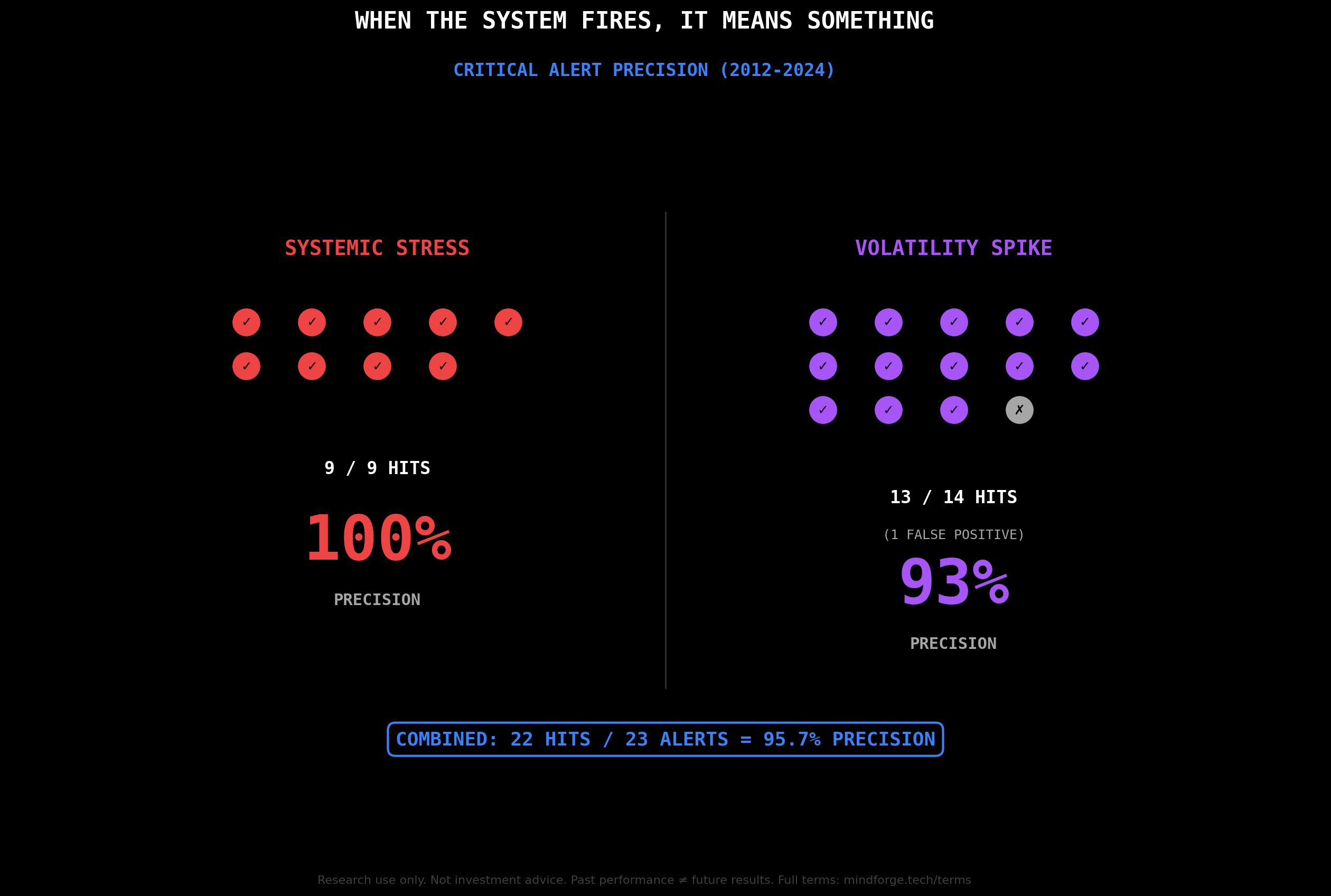

The Precision

Restraint is only a virtue if you catch the actual wolves.

When the system does fire a critical alert:

Zero false positives for Systemic Stress over 13 years.

It caught every confirmed cascade (COVID, August 2024, Q4 2018) without crying wolf on the false alarms (2017, 2023).

One false positive in 23 critical alerts (95.7% total precision).

That’s not luck. That’s architectural discipline.

Why Most Alert Systems Fail

Most systems optimize for sensitivity. They want to catch every event.

The result: alert fatigue. Teams learn to ignore the alerts because they fire too often.

The crying wolf problem

VIX ≥ 25 → ~28 alerts/year

VIX ≥ 30 → ~11 alerts/year

Most don’t matter. Teams stop listening.

Our system fires ~1.8 critical alerts per year (23 over 13 years).

When it speaks, it means something.

2023: The Restraint Proof

In March 2023, SVB collapsed on Friday. Signature Bank was seized on Sunday. First Republic wobbled.

VIX opened Monday around 26 and traded above 30 intraday.

What a threshold system would do

VIX ≥ 25: ALERT

VIX ≥ 30: CRISIS ALERT

Escalate in real time

What our system did

Classified: Turning State (regime inflection)

No Systemic Stress alert

No Volatility Spike alert

The system identified risk, but distinguished it from a cascade.

It said pay attention, not exit.

What happened

VIX closed below 20 by March 28

SPX recovered within days

Market finished the year higher

The banks failed. The system didn’t. The crisis didn’t cascade.

How Do You Build a System That Says “No”?

Not by loosening thresholds.

You build it by demanding the same story across independent measures.

A VIX spike can be hedging demand.

Market weakness can be positioning unwind.

Even both together can resolve quickly.

Critical escalation is reserved for moments when multiple independent measures align and the market behaves like a cascade.

When they do not, the system stays in non-critical states (Turning, Stress) and keeps the critical channel quiet.

2023 had the VIX spike. It did not behave like a cascade.

The system knew the difference.

The Cost of Crying Wolf

Every false alert has a cost:

Direct cost: unnecessary trades, hedging premium, transaction costs

Opportunity cost: missing upside while de-risked

Trust cost: teams stop believing the system

March 2023: a false alert would have de-risked into a strong year.

October 2024: a false alert would have de-risked before the post-election rally.

The system said “no” both times. Both times, correct.

The Real Metric

Most systems report hit rate: “We caught X out of Y events.”

That’s half the story.

The other half: “How often did you fire when nothing happened?”

141:1.

For every critical escalation, we correctly said situation contained about 141 trading days.

Crash detection is table stakes.

Restraint is the edge. Full methodology: https://mindforge.tech/validation-and-methods

Out-of-Sample: 2025

The 2012–2024 window ended. Then came 2025.

In 2025, the system fired two critical alerts:

March 2025: Volatility Spike. Resolved within days.

April 2025: Systemic Stress. VIX hit ~60 (tariff shock). Classified before the cascade.

Two alerts in a full calendar year. Consistent with the ~1.8/year historical average. Zero false alarms.

The restraint held because it’s architectural, not curve-fitted.

Research use only. Not investment advice. Past performance does not guarantee future results. Full terms: https://mindforge.tech/terms

2012–2024 data from validated backtests (systemic_stress_state v5.4.0, volatility_spike_state v1.1.0). 23 critical alerts (9 Systemic Stress, 14 Volatility Spike) over 13 years. Precision: SSS 100% (9/9), VS 93% (13/14). “Critical alerts” refers to Systemic Stress and Volatility Spike states; other states (Turning, Stress) may activate during periods shown as quiet. Backtested performance has inherent limitations. 2025 classifications from observational analysis using production rules. Methodology: https://mindforge.tech/validation-and-methods